ACA Raises Premium Rates For Younger Enrollees, Up To 78% For Some Groups

The Affordable Care Act, or Obamacare as it is commonly known, has been as much political football as it is an actual health insurance marketplace. Now, though, it’s possible to look at the gathered data and come to an understanding of its true effects and impact on the lives (and budgets) of the people who use it.

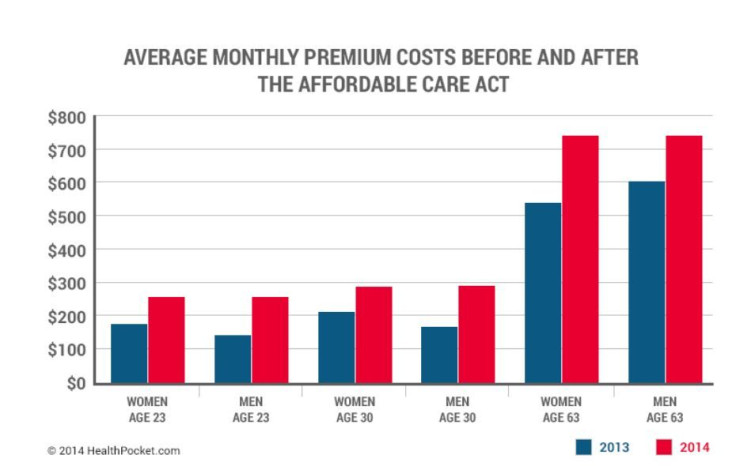

HealthPocket examined average health insurance premiums before the Affordable Care Act was initiated in 2013 and then afterward in 2014. The tech company’s investigation demonstrated a clear increase of average premiums for both sexes and across all age groups in the individually purchased health insurance market. “While the degree of increase varied by age and sex, the occurrence of an increase did not,” wrote Kev Coleman and Jesse Geneson in their new report.

Is It Possible To Make A Direct Comparison?

Among the key principles underlying the regulations of Obamacare was fairness; the law prohibited insurance companies from rejecting anyone due to poor health or increasing their rates over the standard level set for all people their same age, smoking status, and region. To understand the impact of these regulations, HealthPocket gathered the average 2014 ACA premiums for non-smoking men and women ages 23, 30, and 63 and then compared these to averages from the pre-reform individual health insurance marketplace of 2013. (Generally, HealthPocket derives its data from insurance records captured by the Department of Health & Human Services.)

After crunching the numbers, what did the researchers discover? Unsubsidized premiums for an individual health insurance policy increased across all age groups between 2013 and 2014.

The youngest men, those in the 23-year-old age group, had the highest premium increase (78.2 percent) of all, while senior men had the smallest increase (22.7 percent). However, premiums for 63-year-old senior men during 2013 (against which the 2014 increases were calculated to establish the percentage) were the highest of all groups.

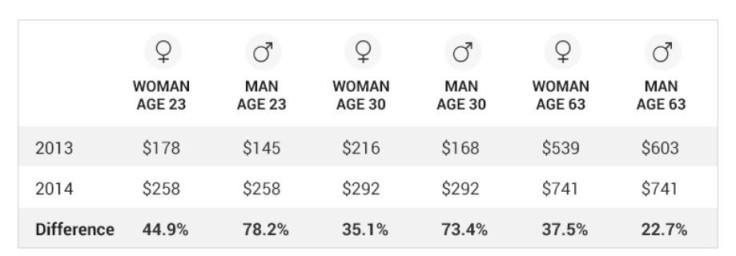

After the new healthcare law went into effect, then, the average premium costs throughout the country for 23-year-old women and men increased 44.9 percent and 78.2 percent, respectively. For 63-year-olds the increase on average was 37.5 percent for women and 22.7 percent for men. Thirty-year old women and men also felt the pinch: their average premiums increased by 35.1 percent and 73.4 percent, respectively.

While the basic premiums for the above percentages were based on nationwide averages, each state has its own average premiums for different age groups and they varied greatly. For example, New York had the highest average monthly premiums for 23- and 30-year-olds ($460 for both groups) during 2014. Conversely, Hawaii had the lowest average monthly premiums for those same two age groups: $190 for 23-year-olds and $216 for 30-year-olds. Vermont ranked as least expensive for average monthly premiums owed by 63-year-olds at $433, while Virginia — which offers plans that, quite unusually, cover gastric bypasses and bariatric surgery — had the highest average monthly premiums for the same age group: $1,101.

“However, the degree to which the cost of consumers’ premiums increased is a more complicated matter than suggested by the premium data,” wrote the authors who explain several matters that confound a simple comparison. One factor is some people now receive subsidies when paying for insurance and another issue is this: Because Obamacare prohibits rejection of applicants based on poor health, what you don’t see in the numbers is the fact that in the pre-reform market nearly one-in-five applications for insurance were rejected. However, many people would argue that before Obamacare, people without insurance simply went to the Emergency Room. Under the law since 1986, hospitals have not been allowed to “dump” patients who lack health insurance and so they must (and do) treat everyone.